Völkischer Beobachter (January 11, 1942)

Die Hauptstadt der Malaienstaaten gefallen

Eine wichtige Barriere vor Singapur durchbrochen

Eigener Bericht des „Völkischen Beobachters“

Zeichnung: „VB.“

dr. th. b. Stockholm, 10. Januar

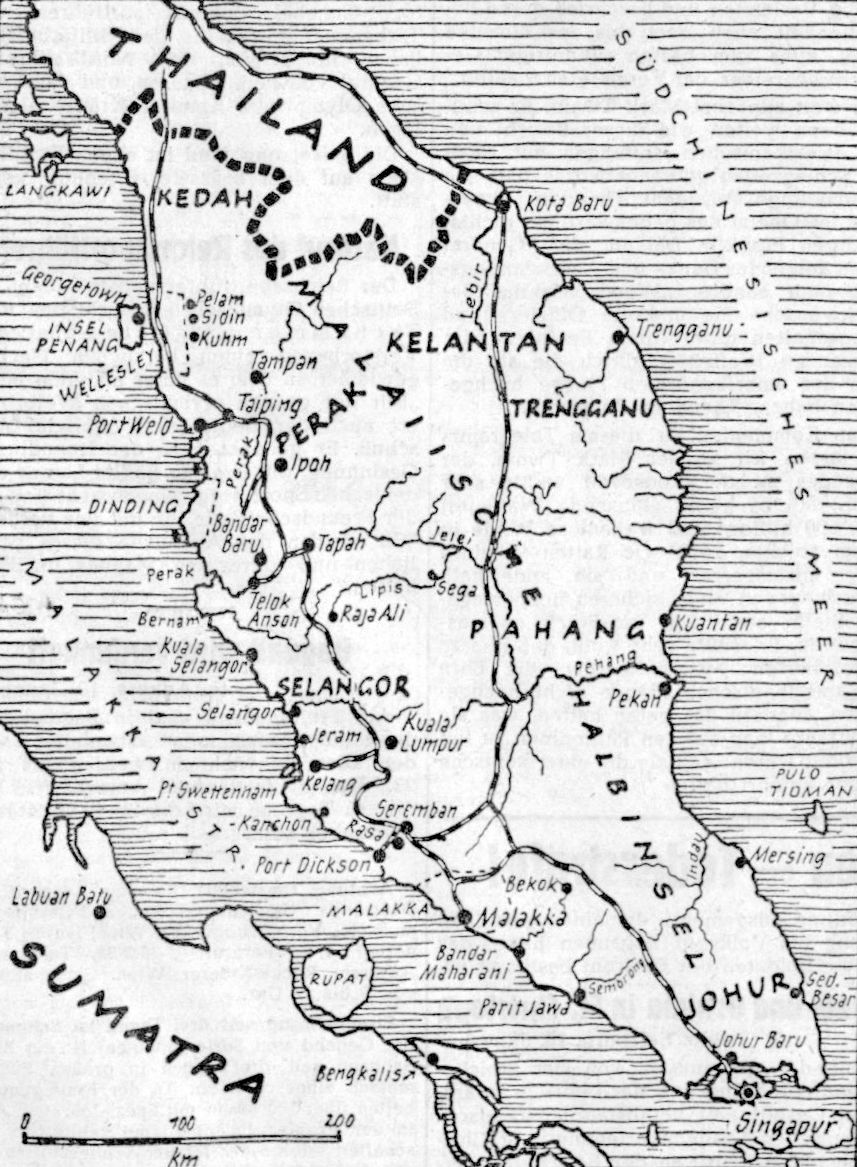

Von der Malayafront kommt soeben die Meldung, daß Kuala Lumpur gefallen ist. Die britischen Truppen haben damit einen weiteren sehr schweren Schlag erlitten. Kuala Lumpur ist die Hauptstadt des Staates Selangor und gleichzeitig die Hauptstadt der vereinigten malaiischen Staaten. Sie hat etwa 150.000 Einwohner. Kuala Lumpur ist der Mittelpunkt des Kautschukhandels auf Malaya. Auch zahlreiche Zinnbergwerke haben dort ihren Verwaltungssitz.

Die Kämpfe um Kuala Lumpur müssen nach Informationen von der Malayafront als die schwersten Kampfhandlungen seit Beginn der dortigen Operationen bezeichnet werden. Sie fanden in einem für die Verteidigung außerordentlich günstigen Gelände statt. Der Feind hatte seit-langem starke Stellungen vorbereitet, teilweise sieben Linien hintereinander, die mit Minen. Tankfallen und Geschützen schwer befestigt waren. Aber all dies hinderte die japanischen Truppen nicht, den Vormarsch unentwegt fortzusetzen.

Nach einer überlegenen Umfassungsoperation, bei der der rechte japanische Flügel vorgezogen wurde und dann in südöstlicher Richtung auf Kuala Lumpur einschwenkte, mußte die britische Verteidigung zurück, wenn sie nicht rettungslos eingeschlossen werden wollte. Die japanischen Truppen wurden durch die Luftwaffe dabei wirkungsvoll unterstützt, die auch in Kuala Lumpur selbst den feindlichen Widerstand heftig bekämpfte. In allen Teilen der Stadt wüteten ausgedehnte Brände. Der größte Teil der Einwohner hatte fluchtartig die Stadt verlassen.

Nach englischen Meldungen spielte sich die entscheidende Schlacht um Kuala Lumpur in dem Dreieck zwischen den Flüssen Slim, Bertram und der Stadt Kuala Lumpur ab. Die Japaner haben hier zum erstenmal Zwölf-Tonnen-Tanks eingesetzt, während sie sich vorher nach englischen Meldungen auf den Einsatz von Zwei-Mann-Tanks beschränkten.

London: „Die Lage sehr ernst!“

„Mehr Soldaten und mehr Flugzeuge, die Lage wird unhaltbar!“ Mit diesen Worten schließt der Sonderberichterstatter des „Daily Herald“ in Singapur seine letzte Meldung. Auch die übrigen Berichte in der Londoner Presse bezeichnen die Lage an der Front als verzweifelt, und im Londoner Nachrichtendienst wurde mitgeteilt, daß zwar noch keine amtlichen Meldungen vorliegen — wahrscheinlich zögert man, den Fall von Kuala Lumpur einzugestehen — daß aber nach allen bisher vorliegenden Berichten die Lage als sehr ernst angesehen werden müsse.

Japanische Flugzeuge, so heißt es in einem Londoner Bericht des „Aftonbladet“, schwärmten durch die Luft und würfen ihre Bomben unbekümmert und ungehindert ab, da so gut wie kein Schuß fiele. Vor den Bomben gebe es keinen anderen Schutz mehr, als sich in den dichten Dschungeln zu verstecken. Ein Berichterstatter der United Press, der sich an der britischen Front befand, gibt folgende dramatische Schilderung: „Ich habe einige Tage auf einem vorgeschobenen Posten in Selangor verbracht und war Zeuge des verzweifelten Kampfes britischer und indischer Soldaten gegen die Übermacht. Die Soldaten mußten in der mörderischen Hitze Übermenschliches ertragen. Überall sieht man bei den Zinnbergwerken zerstörte Maschinen und bei den Kautschukplantagen niedergebrannte Häuser.

Hals über Kopf geflüchtet

Auf den ausgefahrenen, staubigen Straßen wiegt sich ein Strom von hysterischen Menschen, die Hals über Kopf geflohen sind. Viel konnten sie nicht mitnehmen. Viele haben Räder bei sich, die bis zum Brechen beladen sind. Kleine Autos, mit Kindern, Hausgeräten und Konservenbüchsen voll bepackt, versuchen, in lebensgefährlich schneller Fahrt vorwärts zu kommen. Die Angst vor einem japanischen Blitzangriff ist sehr groß, und alle möchten noch schnell nach Singapur kommen. Bei meinem Aufenthalt in den vordersten Linien habe ich mit einem englischen Artilleriehauptmann gesprochen, der mir erzählte, wie plötzlich die japanischen Tanks in den Kautschukplantagen auftauchten, in denen die Japaner jeden Schritt und Tritt kannten. Vielfach wurden die englischen Abteilungen von ihren Verbindungen abgeschnitten. Das Hauptquartier, das ich besuchte, war so schnell verlassen worden, daß die Pfeifen und der Tabak der Offiziere noch auf den Tischen lagen.“

Englands Zerstörungswerk

Das Zerstörungswerk auf der Malaiischen Halbinsel ist das Werk der Engländer, die gleich zu Beginn der Kämpfe nach bolschewistischem Muster den Befehl gaben, alles dem Erdboden gleichzumachen und sich dieser Barbarei in den Berichten aus Singapur noch rühmen. Auch Kuala Lumpur sollte, wie United Press aus Schanghai meldet, niedergebrannt werden. Hier aber kam es zu einem Aufstand der Malaien gegen die britische Polizeitruppe. Die Malaien bewaffneten sich und eröffneten auf englische Polizisten und indische Soldaten, die sich an der Vernichtung der Stadt beteiligt hatten, das Feuer.

Eine Heldentat aus der Kolonialgeschichte der USA

Roosevelt „befreit“ die Philippinen

Eigener Bericht des „Völkischen Beobachters“

vb. Wien, 10. Januar

Nach der Eroberung Manilas durch die Japaner, die praktisch den Zusammenbruch der amerikanischen Herrschaft auf den gesamten Philippinen bedeutet, hat Präsident Roosevelt, wie berichtet, an die Bewohner der Inselgruppe ein gefühlvolles Telegramm gerichtet. Er beklagte von tiefem Herzen, daß die USA außerstande gewesen seien, dem japanischen Angriff erfolgreichen Widerstand zu leisten, versprach jedoch den Filipinos, daß Amerika sie zu gegebener Zeit „befreien“ werde.

Wir möchten bezweifeln, ob die Filipinos sich nach dieser Befreiung sehnen. Nach den Erfahrungen, die sie mit den USA gemacht haben, ist das wenig wahrscheinlich. Die Geschichte der amerikanischen Herrschaft auf den Philippinen füllt wirklich keine rühmlichen Seiten im auch sonst nicht fleckenlosen Buche der amerikanischen Vergangenheit. Feuer und Schwert standen am Anfang der amerikanischen Machtergreifung über den Inseln, plutokratische Ausbeutung am Ende. Am Anfang und am Ende aber stand der Name: Roosevelt.

Die Philippinen waren früher bekanntlich spanischer Besitz. Als die USA gegen Spanien in den letzten Jahren des vorigen Jahrhunderts einen Krieg Vom Zaun gebrochen hatten, der zunächst der Eroberung von Kuba galt, wuchs ihr Appetit mit dem Essen, und sie ließen sich von dem besiegten Gegner beim Friedensschluß auch die Philippinen abtreten. Damit waren die Inseln wohl Eigentum, aber noch nicht Besitz der USA geworden, denn die Einwohner zeigten keine Lust, den neuen Herrn gegen den alten einzutauschen.

Es ist nie besonders erfreulich, in der schmutzigen Wäsche anderer Nationen herumzustochern, und so verzichten wir darauf, mit unseren Worten eingehend zu schildern, wie die Amerikaner die Philippinen „befreiten“. Wir geben das Wort dem bekannten amerikanischen Schriftsteller Mark Twain. Er war einer der wenigen Amerikaner, die sich innerlich über die Methoden der Kolonialpolitik ihres Landes empörten. In seiner Selbstbiographie (Neuyork und London 1924) schildert er im 2. Bande auf Seite 186 ff. eine der übelsten Greuelszenen der amerikanischen Kolonialimperialisten. Sie spielt, das verdient Beachtung, im Jahr 1906, also nach acht Jahren, nachdem die Amerikaner auf den Philippinen Fuß gefaßt hatten. Mark Twain berichtet über die „Schlacht von Jolo“ wörtlich folgendes:

„Montag, 12. März 1906. Ein ganzer Stamm dunkelhäutiger Eingeborener, sogenannter Moros, Männer, Weiber und Kinder, hatte sich in der Tiefe eines erloschenen Kraters verschanzt, wenige Meilen von Jolo, und da sie uns feindlich gesinnt und wir seit Jahren darauf aus waren, ihnen ihre Freiheiten zu nehmen, war ihr Aufenthalt dort für uns eine Drohung. Unser Befehlshaber, General Leonard Wood, schickte einen Spähtrupp vor: der stellte fest, daß die Moros sechshundert an Zahl waren, Weiber und Kinder eingerechnet, und daß ihr Krater sich zweitausendzweihundert Fuß hoch über dem Meeresspiegel in dem Gipfel eines Berges befand und für weiße Truppen und Artillerie sehr schwer zugänglich war. General Wood ordnete einen Überfall an und ging auch selber mit, um sich die Ausführung seines Befehls anzusehen.

600 Filipinos erbarmungslos abgeschlachtet

Unsere Truppen erklommen die Höhen auf gewundenen und schwierigen Pfaden und nahmen auch Artillerie mit. Was für Artillerie, ist nicht näher angegeben, aber an einer Stelle, einer scharfen Steigung von etwa dreihundert Fuß, mußte sie durch einen Flaschenzug hinaufgewunden werden. Kaum war man am Rande des Kraters angelangt, so begann die „Schlacht“. Unserer Soldaten waren fünf hundert und fünfzig. Zu ihrer Unterstützung waren ihnen ein Detachement der von uns in Sold genommenen einheimischen Polizeitruppe und ein Marinedetachement beigegeben, deren Zahlen nicht angegeben sind. Allem Anschein nach war aber die Zahl der Streiter auf beiden Seiten ungefähr gleich: sechshundert Mann auf unserer Seite oben auf dem Rande des Kraters, sechshundert Männer, Weiber und Kinder unten in der Tiefe des Kraters. Tiefe des Kraters fünfzig Fuß.

General Woods Befehl war: Die sechshundert töten oder gefangennehmen. Also die „Schlacht“, wie sie amtlich genannt wird, begann, die unsern mit ihrer Artillerie und ihren todbringenden modernsten Handfeuerwaffen in den Krater hinunterfeuernd, die Wilden das Feuer von unten herauf wütend erwidernd: Wahrscheinlich mit Steinen, doch ist das nur eine Vermutung von mir, da die Waffen, deren sich die Wilden bedienten, in dem Kabeltelegramm nicht genannt sind. Bis da- hin waren bei ihnen nur Messer und Keulen und unbrauchbare Schießprügel, wenn sie welche hatten, in Gebrauch gewesen.

Der amtliche Bericht stellte fest, daß die „Schlacht“ auf beiden Seiten mit ungeheurer Energie ausgefochten worden sei, daß sie einen und einen halben Tag gedauert und mit einem vollständigen Sieg der amerikanischen Waffen geendet habe. Die Vollständigkeit des Sieges wird durch die Tatsache, daß von den sechshundert Moros nicht einer am Leben geblieben ist, der Glanz des Sieges durch die Tatsache, daß von unseren sechshundert Helden nur fünfzehn ums Leben gekommen sind, außer Zweifel gestellt.

General Wood war dabei und sah zu, sein Befehl war gewesen: die sechshundert töten oder gefangennehmen. Unsere kleine Armee hat dieses „oder“ offenbar so aufgefaßt, als habe er es ihr anheimgestellt, ganz nach Belieben zu töten oder gefangenzunehmen, und ihr Belieben war dasselbe geblieben, daß es bei unserer Armee dort draußen acht Jahre lang gewesen war: das Belieben christlicher Metzger.

Der amtliche Bericht, wie sich das gehört, strich das „Heldentum“ und die „Tapferkeit“ unserer Truppen heraus und vergrößerte sie noch, beklagte die fünfzehn, die umgekommen waren, verbreitete sich über die Verwundungen der zweiunddreißig Verletzten und beschrieb deren Beschaffenheit auch noch bis ins einzelne genau, alles zum besten zukünftigen Geschichtsschreiber der Vereinigten Staaten.“ Soweit zunächst Mark Twain. Er schildert dann weiter, wie dieser Bericht von den amerikanischen Zeitungen mit riesigen Schlagzeilen gebracht wurde und wie der damalige Präsident Theodore Roosevelt, der Oheim des gegenwärtigen nichtswürdigen Franklin Delano, dem General Wood folgendes Dank- und Anerkennungstelegramm sandte: „Wood, Manila. Beglückwünsche Sie und die Offiziere und Mannschaften unter Ihrem Befehl zu der glänzenden Waffentat, durch die sie die Ehre der amerikanischen Flagge hochgehalten haben. Theodore Roosevelt.“

Den Kommentar zu diesem Telegramm überlassen wir wieder Mark Twain, der folgendes meint: „Roosevelt wußte sehr wohl, daß es keine glänzende Waffentat war, 600 hilflose und waffenlose Wilde in einem solchen Loch wie Ratten in einer Falle einzusperren und sie anderthalb Tage lang von einer sicheren hochgelegenen Stelle aus Stück um Stück zu massakrieren. Er wußte sehr wohl, daß unsere uniformierten Meuchelmörder die Ehre der amerikanischen Flagge nicht hochgehalten, sondern das getan hatten, was sie acht Jahre lang auf den Philippinen zu tun gewohnt waren: daß sie die amerikanische Flagge entehrt hatten.“

Roosevelts Rüstungsprogramm

„Sei nicht so undankbar — du siehst doch, was sich der Onkel für Mühe gibt!“

Mit unbekanntem Ziel ausgelaufen:

Die britische Flotte verläßt Singapur

Eigener Bericht des „Völkischen Beobachters“

rd. Rom, 10. Januar

Die aus Saigon kommende Meldung, daß die englischen Kriegsschiffe, die bisher vor Singapur tagen, den Hafen der britischen Festung im Morgengrauen unter mörderischem Feuer der Flakbatterien gegen nicht vorhandene japanische Flugzeuge verlassen haben, wird in Rom als eine der nicht nur militärisch aktuellen, sondern geschichtlich bedeutsamsten Nachrichten seit Ausbruch des Krieges im Pazifik bezeichnet.

Das Geschwader hat britischen Angaben zufolge Kurs „auf einen unbestimmten Punkt“ genommen, um sich dort unter den Befehl des amerikanischen Generals Hart zu stellen. Vermutlich heißt der unbestimmte Punkt Surabaya auf Java, wo sich auch die Reste des USA-Ostasien-Geschwaders zu konzentrieren suchen.

Über die Gefühle, mit denen man in England das bisher noch nie dagewesene Schauspiel der Übernahme des Oberbefehls über britische Flottenteile durch einen nichtbritischen Admiral beobachtet, hat die letzte Unterhaussitzung mit den in den Vereinigten Staaten „als wenig elegant“ bewerteten Bemerkungen Sir George Geoffreys genügend Aufschluß gegeben. Die andere Seite des Vorganges der Flottenflucht aus Singapur ist nach römischem Urteil das Eingeständnis Londons, daß es fürchtet, die Festung könnte bald auch zur See blockiert werden. Singapur wurde gebaut, um den plutokratischen Flotten in Ostasien eine Basis zu geben, nun wird Singapur eine Basis ohne Flotte.

Nach der gleichen Quelle haben die Engländer, um die japanischen Bomber irrezuführen, mit Lichteffekten, die den Stadtplan der britischen Festung nachahmen, im Norden der Festungsinsel ein „zweites Singapur“ in den Dschungel gebaut. Die Japaner haben den Engländern aber nicht das Vergnügen bereitet, auf diesen Trick hereinzufallen.

„Tokio Asahi Schimbun“:

Das Empire zerfällt

dnb. Tokio, 10. Januar

Zu der letzten Sitzung des britischen Parlaments meint „Tokio Asahi Schimbun“ ironisch, es sei wohl reichlich spät, jetzt über die ungenügenden Verteidigungsmaßnahmen in Malaya zu debattieren. Die politische Verantwortung für die Überschätzung der eigenen Kräfte, die Unterschätzung der japanischen Kampfstärke und das Vertrauen auf die USA-Hilfe müßten die britische Regierung, das Parlament und die englische Presse schon gemeinsam tragen.

Australiens Haltung verursache in London anscheinend besondere Kopfschmerzen. Wenn England nicht Kraft genug besitze, um Australien als Mitglied des Empire zu schützen, so sei als natürliche Folge damit zu rechnen, daß sich Australien künftig nicht nur militärisch, sondern auch politisch an die USA anlehne. Das Verhältnis zwischen USA und Australien zeichne den Weg vor, der vor dem britischen Empire liege, nämlich der eines unaufhaltsamen Auseinanderfallens, während gleichzeitig die USA die Nachfolgerschaft anträten.

Noch im letzten Jahr sei Churchill voll Stolz und Siegeszuversicht von der sogenannten Atlantikkonferenz zurückgekehrt. Es bleibe abzuwarten, mit welchen Gefühlen er diesmal von der Washingtoner Besprechung nach London zurückkomme.

Das Hauptquartier der Marine gibt bekannt, daß bis zum 8. Januar aus dem Hongkong-Bezirk folgende Meldungen über vernichtete, beziehungsweise erbeutete feindliche Schiffe vorliegen:

Versenkt: Ein Zerstörer, vier Kanonenboote, sieben Torpedoboote, ein Öltanker, zwei Minenleger, acht Patrouillenboote.

Erbeutet: 110 größere und kleinere Handelsschiffe.

Ernstlich bedrohte Versorgung

Eigener Bericht des „VB“

dr. th. b. Stockholm, 10. Januar

Major Lloyd George vom englischen Ernährungsministerium erklärte, daß der Krieg in Ostasien zu einer fühlbaren Einschränkung der Lebensmittelversorgung führen werde. Amerikanische Dampfer seien jetzt den gleichen Angriffen ausgesetzt wie britische. Die Bevölkerung werde sich mit dem Gedanken vertraut machen müssen, den Riemen noch enger zu schnallen.